The Two-Day Delay Inside the Bond Market

Most people think of a bond transaction as a single moment — a company or government raises money, investors buy in, done. What they don’t see is the machinery running underneath it.

I spent two years at Bank of America executing debt capital markets transactions for sovereign governments and institutional issuers across Southeast Asia — the Republics of Indonesia and the Philippines, Temasek, Khazanah, and major regional corporates. Over that time I helped execute over US$14 billion in bond issuances. And the longer I worked in that machinery, the more one question kept surfacing: why is this still so slow?

The problem nobody talks about

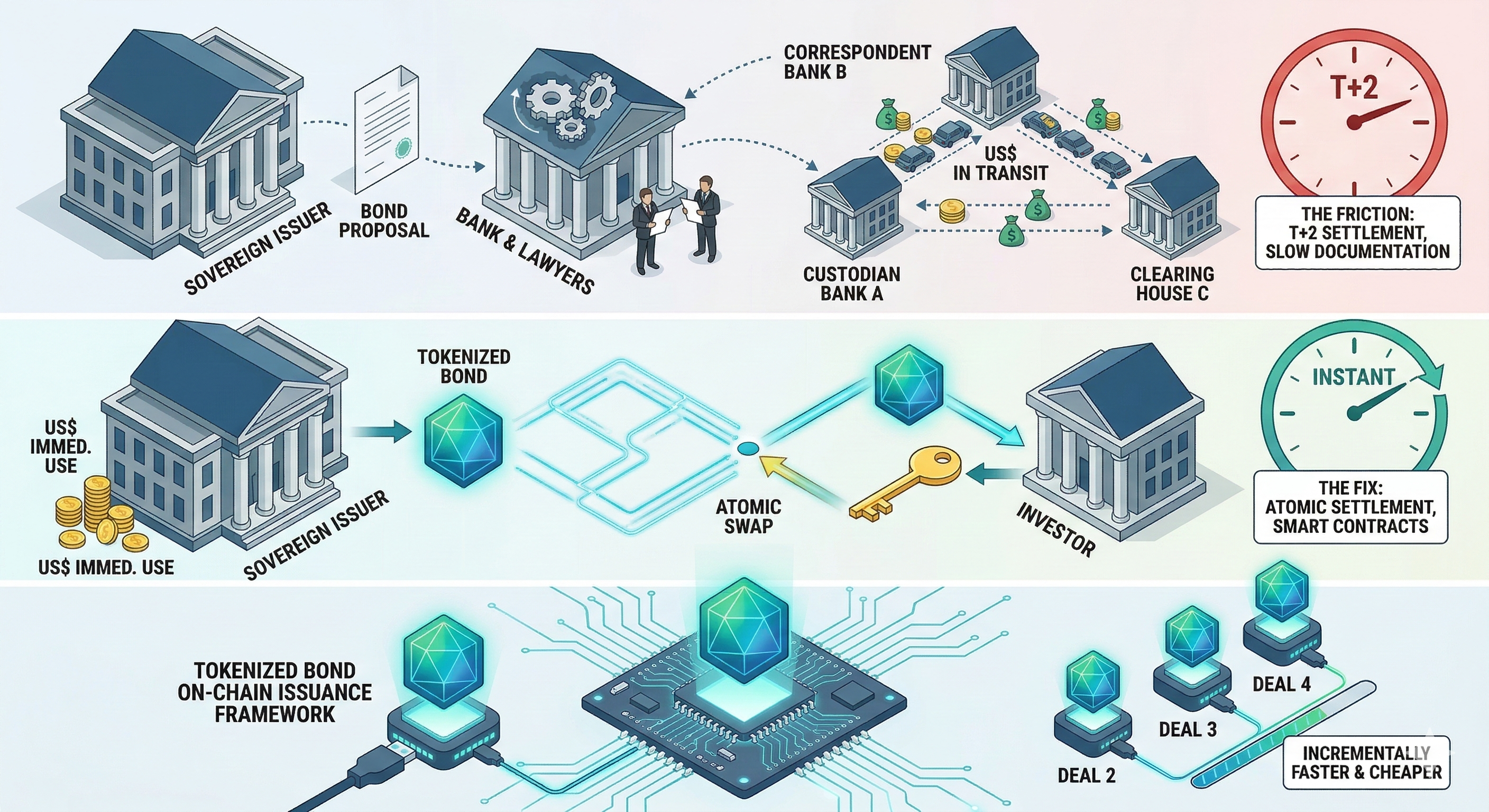

When a sovereign government raises US$3 billion in the bond market, the transaction doesn’t settle the moment the books close. It settles T+2 — two business days later. During those two days, the capital is in transit. It has been committed by investors but hasn’t reached the issuer. Nobody can use it. It simply sits, moving through a chain of custodians, correspondent banks, and clearing houses, each confirming to the next that yes, the cash is coming.

For a treasurer managing national liquidity, two days of dead capital on a multi-billion dollar transaction is a meaningful cost. Multiply that across every bond issuance, every coupon payment, every redemption, and the inefficiency compounds into something significant.

The documentation process is no faster. Before any transaction can go live, the legal team — external counsel, bank counsel, issuer counsel — spends a minimum of two weeks drafting and negotiating the Offering Circular. This is the legal backbone of the bond: the covenants, the representations, the conditions precedent, the events of default. Every term is negotiated line by line. Every version is reconciled manually across multiple parties. I spent hours auditing these documents to ensure that what the lawyers wrote matched what the bank had agreed, what the issuer had approved, and what the regulators required. A single misaligned clause could delay a transaction or expose the bank to liability.

Two weeks of legal preparation. Two days of settlement lag. Months of post-issuance record-keeping distributed across six or seven institutions, each maintaining their own version of the same ledger.

This is the infrastructure underpinning the global bond market.

What tokenization actually fixes

When I started studying RWA tokenization seriously, what struck me wasn’t the technology — it was the precision with which it targets exactly these two problems.

Atomic settlement eliminates the T+2 gap entirely. On a blockchain, delivery versus payment happens simultaneously within the same transaction. The bond token transfers to the investor at the exact moment the cash transfers to the issuer. There is no two-day window, no chain of correspondent banks, no capital sitting in transit. For a sovereign treasurer managing national liquidity across multiple concurrent obligations, the capital efficiency implications are significant.

Smart contracts address the documentation overhead differently. Rather than a 200-page Offering Circular negotiated by three sets of lawyers, the covenant structure is encoded directly into the token. Transfer restrictions, payment conditions, compliance requirements — these are enforced automatically at the protocol level, not audited manually after the fact. The blockchain becomes the golden record that every party reads from simultaneously, replacing the distributed reconciliation process where six institutions maintain six versions of the same truth.

Even for repeat issuers returning to market for the fifth or tenth time, the documentation process largely resets. The Offering Circular is copied, marked up, negotiated, and re-executed which is a process that takes weeks regardless of how familiar the parties are with each other. Tokenization changes this dynamic fundamentally. Once a sovereign issuer establishes their on-chain issuance framework, subsequent deals update parameters within an existing smart contract rather than rebuilding the legal architecture from scratch. The first deal is the heavy lift. Every deal after that is incrementally faster and cheaper.

Why I’m convinced

Of the two, atomic settlement is where I see the most immediate and tangible value — specifically for institutional treasurers.

In traditional DCM, the two-day settlement window is so normalised that most practitioners don’t question it. It’s just how it works. But when you’ve sat across the table from a sovereign treasury official managing the funding needs of an entire nation, and you understand the precision with which they manage their liquidity position, the idea of giving them back two days of capital efficiency on every transaction isn’t incremental — it’s meaningful.

The infrastructure to deliver this is no longer theoretical. BlackRock’s BUIDL fund settles transactions on-chain. MAS Project Guardian is piloting tokenised bond issuance with major institutions in Singapore. The regulatory framework is being built in parallel with the technology.

The friction I watched slow down billion-dollar transactions for two years has a structural solution. That’s why I’m here.

A year ago I was coordinating settlement confirmations across six banks for a sovereign bond that took two days to clear. The technology that makes that two-day wait unnecessary already exists. The framework to deploy it at sovereign scale is being built right now. I left traditional Capital Markets because I wanted to be on the side building what comes next — not managing the inefficiency of what came before

-- End --