Grow a Stablecoin Playbook for Issuers, Institutions, and Builders

Thesis: Stablecoin success is a distribution + liquidity + trust problem, not just a technical or branding problem; winners are those that plug into existing financial channels, meet regulatory expectations, and deliver clear economic value to each participant in the network.

About E8

E8 was founded by data-driven Web3 and banking professionals with direct experience at OKX, Spartan Group, Binance, GIC, and Bank of America, who have weathered the industry's full cycle across traditional finance and DeFi. We hope to produce thoughtful articles, trends analysis, and actionable growth playbooks that can add value to founders, institutions and the community itself.

E8 is committed to help Web3 projects scale exponentially through battle-tested strategies and relentless execution.

In the past 2-3 years, the industry has witnessed an explosive growth in stablecoins. They have already moved from a crypto niche to a core payment infrastructure and drew serious attention from major financial institutions and fintech players.

In this short article, we hope to break the stablecoin growth problem into a few core pieces: distribution, liquidity, trust, and regulation. We are sharing this playbook as a resource for those looking to either issue or integrate a stablecoin.

1. Distribution as the primary moat

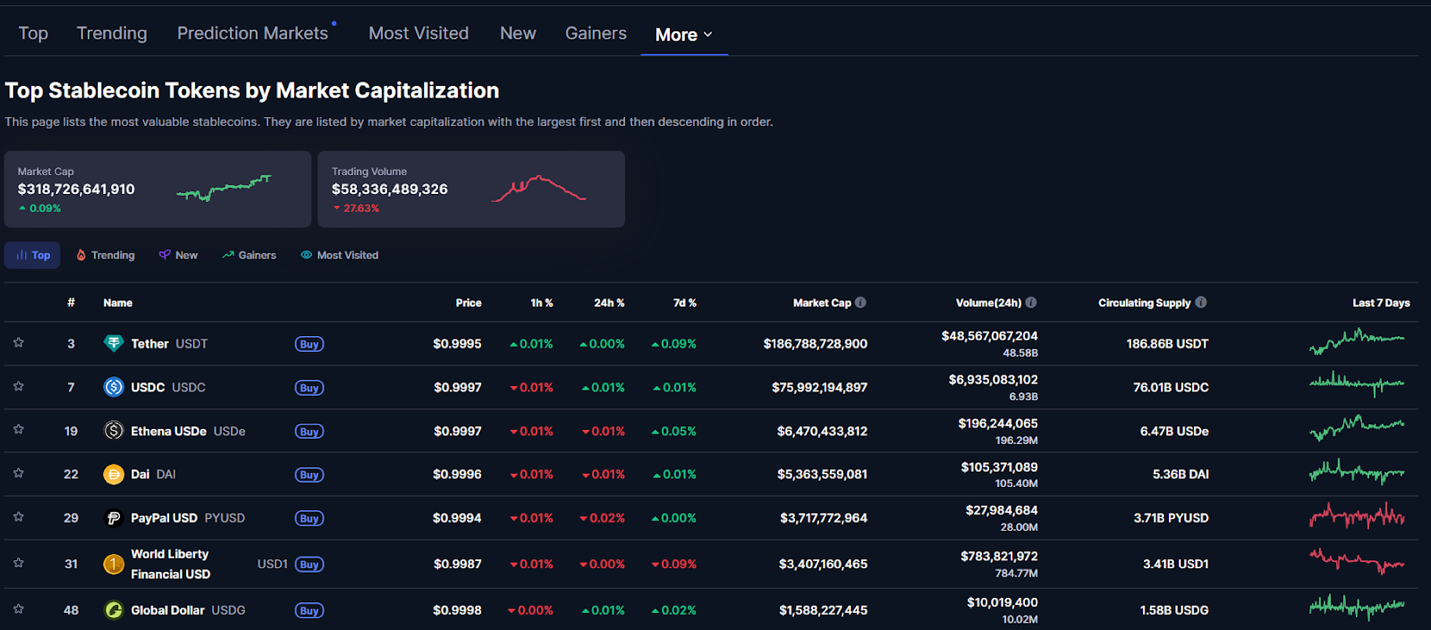

There are over 276 stablecoins in the ecosystem but it is common for users to be only using USDT, USDC and USDe. Why do most stablecoins find it difficult to grow?

Stablecoin growth is fundamentally a distribution problem. The technology, yield or branding does not matter if the stablecoin does not have a path of least resistance. This means a pathway where value currently moves, and the destination it needs to go.

USDT became dominant because it was available to everybody. Traders, remitters and operating merchants were all using it, creating a self-reinforcing network effect.

The key principle behind this distribution compounds across 3 layers in our view: trading venues, consumer-facing apps and real world payment flows.

| Layer | Why it matters | Example |

|---|---|---|

| Trading Venues | 70-80% of stablecoin volume is trading-related. A deeper book will result in tighter spread. | USDT on Binance, OKX (traders); USDC on Coinbase, Kraken (institutions) |

| Wallets & Apps | Where users hold and send money daily. It creates “stickiness”. Users generally don’t change wallet. | USDT in Phantom, MetaMask; USDC in PayPal, Stripe Checkout |

| Payment Flows | Where stablecoins replace wires/cards. This venue has highest revenue per user. | USDC settlements via Circle's API / PYUSD merchant payments etc |

Next, how do we at least achieve Product Market Fit (PMF) in one of the layers? The network effect of a stablecoin cascades once it has distribution in one layer. A prime example would be PYUSD.

Case Study: PYUSD

- Consumer facing App (Paypal/Venmo): PYUSD launched in November 2023 and integrated directly into the PayPal ecosystem, granting over 400 million users and Venmo customers immediate access. This allows users to seamlessly buy, hold, and transfer PYUSD using their existing account balances. This helped them grow from $0 to $100M market cap in 3 months through their existing payment retails.

- Self-reinforcing liquidity in CEX/DEX: When PYUSD gained retail traction, it was then listed by Coinbase, Kraken and Binance. Securing these top-tier listings usually requires a combination of high organic volume, rigorous regulatory compliance, and a proven track record of reserve transparency. The daily trading volume then hit $4B by Q1 2025.

- UX Pathways across channels: Wallets such as Phantom, MetaMask, Solana Pay integrated PYUSD. DeFi protocols (Kamino and Jupiter) added PYUSD pools. On a merchant level, Blackhawk Network (gift cards), Bitrefill (mobile top-ups) started accepting PYUSD payments via PayPal checkout.

PYUSD remains sticky because merchants using PayPal's existing PYUSD checkout rarely switch because it leverages PayPal's fraud protection, dispute resolution infrastructure. This shows that the flywheel works.

TL;DR: Dominate one layer → attract liquidity → cascade across layers → build moat.

2. Liquidity strategy: where and how to seed

For any new stablecoin, the fundamental cold-start problem is liquidity. Users read depth and tight spreads as a proxy for confidence in the ecosystem. Traders and integrators want to see deep, reliable books before routing meaningful size through an asset, while liquidity providers want to see real traction before committing capital. If neither side moves first, the peg and the entire swapping experience become fragile, and adoption stalls.

2.1 Why deep, reliable liquidity is non-negotiable

Liquidity is more than a nice-to-have; it is what turns a “token” into something that behaves like money. Deep, reliable liquidity:

- Compresses spreads

- Lowers price impact for larger orders, improving UX for both retail and institutional users.

- Makes it operationally safe for protocols, PSPs, and treasuries to integrate the stablecoin as core infrastructure.

On CEXs, a deep order book with tight bid-ask spreads signals that market makers are confident enough to warehouse risk in your stablecoin. In DeFi, well-funded stable swap pools (e.g., Curve-style AMMs) enable low-slippage swaps even for size, which is critical for maintaining the peg and making integrations viable

2.2 Crypto-native playbook: bootstrapping via DeFi

For DeFi-native stablecoin projects, the first battleground is usually on-chain.

a) Use incentives to kickstart your core pools

- Launch liquidity mining programs for LPs in key pairs (e.g., your stablecoin vs USDC/USDT) on DEXs like Curve or Uniswap, layered on top of swap fees.

- Structure rewards as points, protocol tokens, or revenue share to attract initial TVL. The goal is not just “big TVL”, but enough depth to make trades feel frictionless.

Research on liquidity mining shows that, when done well, incentives can create a liquidity → volume bootstrapping effect: temporary incentives pull in liquidity, which improves pricing and UX, which then drives organic trading volume, leaving the pool at a higher equilibrium even after incentives are reduced.

b) Partnering with active funds and market makers

Pure retail farming often produces mercenary capital.

- The team needs to bring in active liquid funds/market makers early with structured agreements (e.g., minimum depth commitments in return for discounted fees or token allocations).

- Use them as a backstop during volatile periods, so users don’t see wild slippage or broken pegs on day one.

c) Designing stable swap pools to be frictionless

For stablecoins, venue choice and pool design matter as much as raw dollar TVL:

Use stable-optimized AMMs (Curve-style) that minimize slippage for pegged assets, with low base fees (often <0.1%) to make swaps cheap and frequent.

Subsidize these pools heavily in the early months, then gradually taper incentives as organic volume and fee revenue grow.

One good example would be what Gauntlet did on Optimism. The liquidity bootstrapping flywheel effect was successful for wstETH/WETH:TVL market share skyrocketed during the experiment, leading to a big boost in fees, leading to significant boost in TVL and fees after the experiment. For this pool, the liquidity mining program transformed it from almost completely dormant to a fairly active state.

2.3 Web2.5 / institutional playbook: CEX, prime, and OTC rails

The second approach is more web2.5: leaning on centralized venues and institutional infrastructure.

a) Centralised exchanges (Tier-1 CEXs)

- Listings on major CEXs (Binance, OKX, Coinbase, etc.) immediately plug your stablecoin into global liquidity and fiat on/off-ramps. But the real objective isn’t just a ticker, it is getting exposure and market makers to ensure liquidity for the protocol.

- Securing designated market makers to maintain deep two-sided books in your main pairs (e.g., stablecoin/USDT, stablecoin/USDC, stablecoin/BTC).

- Negotiating reasonable maker/taker fees and possibly market-making support programs to incentivize depth.

b) Prime brokers and off-exchange OTC

Prime brokers and OTC desks bridge your stablecoin into block-size, relationship-driven liquidity:

- They handle large flows from funds, corporates, and whales without moving the screen price, which keeps visible markets stable.

- They also help with cross-venue arbitrage, tightening spreads between CEX, DEX, and regional exchanges.

This off-exchange channel is critical if you want your stablecoin to be used in institutional treasury operations rather than just retail trading.

c) Using pre-funding and float to your advantage

Some payment providers now use stablecoin pre-funding to offer 24/7 liquidity and same-day settlement for cross-border flows, reducing the need for nostro/vostro balances. If your stablecoin is part of these pre-funding arrangements (e.g., with PSPs or remittance networks), you effectively lock in recurring, non-speculative demand.

The goal of your liquidity strategy is simple: make every interaction with your stablecoin feel uneventful. When users, traders, and treasurers stop thinking about execution risk and just treat your token as money, you won the liquidity battle.

-- End --